Building a financial backup plan is essential in today’s uncertain world. This Emergency Fund Guide helps you create a strong financial safety net before life becomes stressful. It can support you during job loss, medical emergencies, urgent home repairs, sudden car costs, or family needs. In this article, you will learn how to build, manage, and grow emergency savings through simple steps, smart planning, and consistent action.

What Is an Emergency Fund and Why Do You Need It?

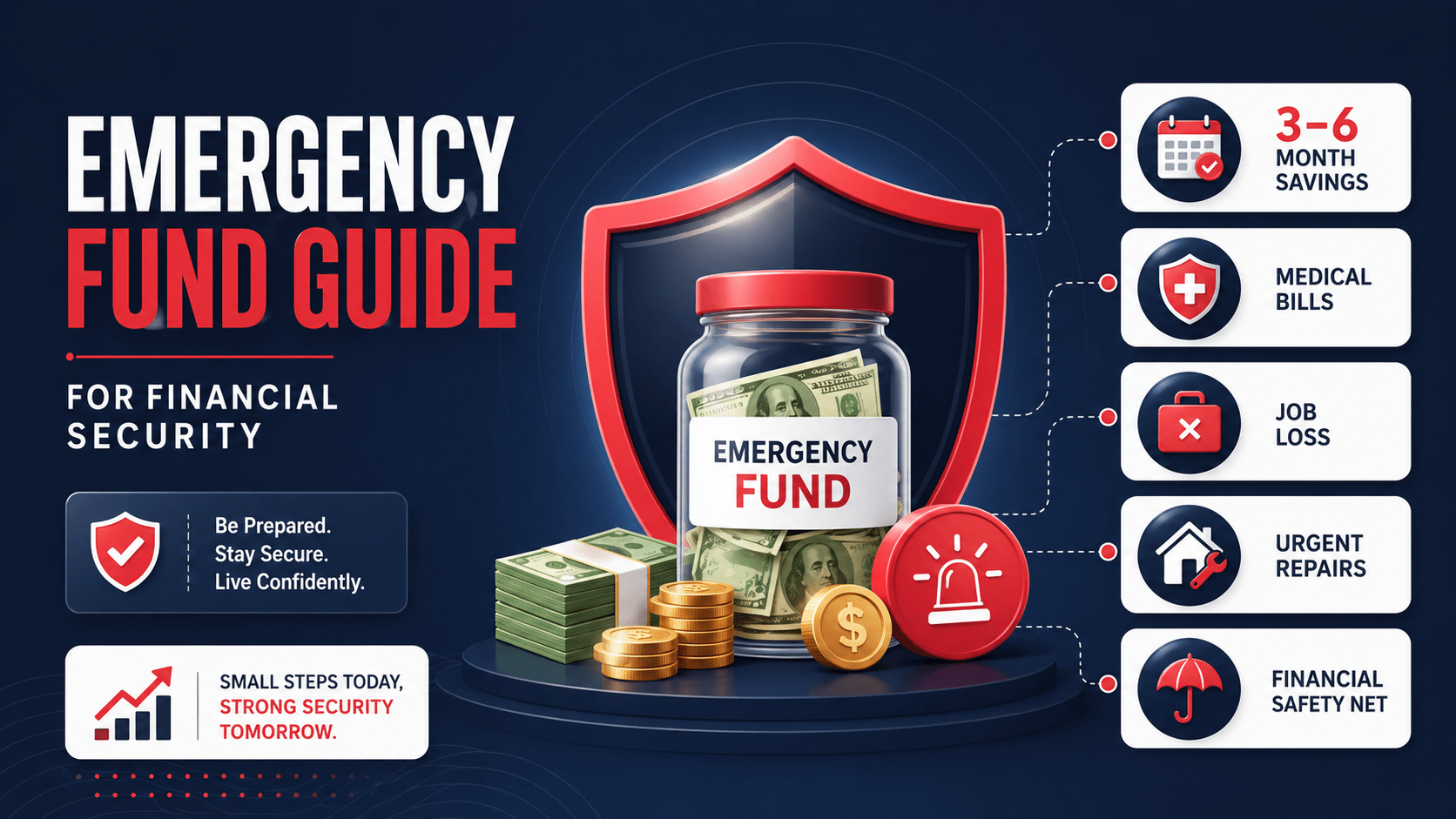

An emergency fund is money you save only for unexpected expenses. It is not for vacations, shopping, or regular monthly spending. It works as emergency savings that protect you when your income or normal budget cannot cover sudden costs. This financial safety net can help with medical bills, job loss, urgent repairs, or important family needs without forcing you to borrow money.

You need this fund because life can change without warning. Without savings, one problem can create debt, stress, and long-term financial pressure. A strong financial safety net gives you confidence, protects your budget, and supports long-term security. This Emergency Fund Guide also helps you build better personal finance habits so you can stay prepared and make calmer decisions during difficult times.

How Much Emergency Fund Should You Have?

The right amount depends on your income, monthly expenses, lifestyle, dependents, and job stability. A clear target makes saving easier because you know exactly what you are working toward. You can also use an emergency fund calculator to estimate your basic savings goal before creating your monthly plan.

- A 3 month emergency fund works well if your income is stable.

- A 6 month emergency fund is safer if your income is uncertain.

- Monthly expenses decide your base savings target.

- Dependents and lifestyle can increase your required amount.

- Job risk level affects how much protection you need.

- Self-employed people may need a larger safety fund.

Start small and build slowly. You do not need to save the full amount at once. Even weekly savings can move you closer to your goal. Review your target when your rent, income, bills, or family needs change. This Emergency Fund Guide focuses on realistic planning, steady growth, and long-term consistency.

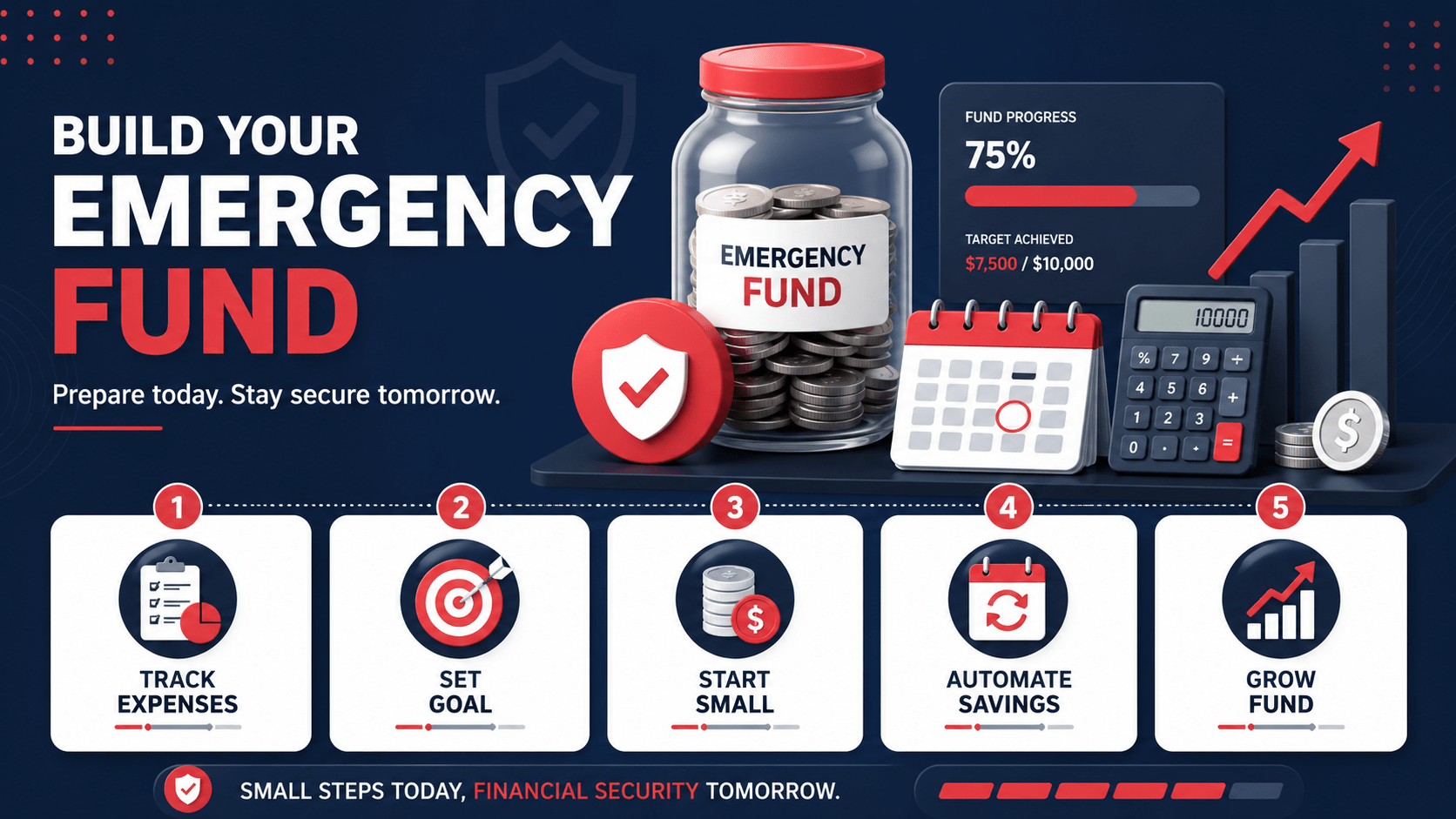

Step-by-Step Emergency Fund Guide: How to Build It

You can start building emergency savings by checking your real monthly expenses. Track rent, food, utilities, transport, insurance, subscriptions, and debt payments for one month. This helps you understand your spending and create a simple savings plan that fits your income.

Next, set a realistic goal and divide it into smaller targets. If you want to know how to build an emergency fund, begin with $500 or $1,000. After that, work toward three to six months of essential expenses. Smaller targets feel easier and help you stay motivated.

Automation can make saving easier. Send a fixed amount to your fund every payday, even if the amount is small. This Emergency Fund Guide works best when you focus on regular action instead of waiting for extra money. Keep the plan simple, review it monthly, and increase your savings amount whenever your income improves.

Smart Savings Plan: Tips to Grow Your Emergency Savings Faster

A smart savings plan helps you grow emergency savings without feeling overwhelmed. You do not need a very high income to succeed. You need discipline, clear priorities, regular action, and patience. Small financial changes can create strong results when you repeat them every month and avoid unnecessary spending.

- Automate savings every month or every payday.

- Cut unnecessary expenses like unused subscriptions.

- Use bonuses, tax refunds, or windfalls wisely.

- Start a side income for extra cash.

- Apply budgeting strategies to control spending.

- Follow practical money saving tips daily.

- Avoid impulse buying and review your budget often.

If you save extra income instead of spending it immediately, your fund will grow faster. A simple personal budget can also help you control spending and reduce waste. This Emergency Fund Guide helps you stay focused, protect your progress, and build stronger habits for future stability. You can learn more about our publishing purpose on the About USA Top Guest Post Site page.

Where to Keep Your Emergency Fund for Safety and Accessibility

You should keep emergency savings in a place that is safe, liquid, and easy to access. The main goal is not high profit. The main goal is quick availability during a real emergency. If the money is difficult to withdraw, it may not help when you need support immediately.

A regular savings account is a good starting point for beginners. A savings account can keep money separate from daily spending while still allowing access. High-yield savings accounts may offer better returns with low risk. Money market accounts may also provide flexible access for some savers.

Avoid risky investments for this fund. Stocks, crypto, or long-term investment accounts can lose value or become hard to access when you need money quickly. This Emergency Fund Guide recommends keeping emergency money simple, protected, and ready for urgent use. This Emergency Fund Guide also suggests choosing an account you understand, so you can avoid confusion during stressful moments.

| Option | Risk Level | Accessibility | Best For |

| Savings Account | Low | High | Beginners |

| High-Yield Savings | Low | High | Better returns |

| Money Market Account | Low–Medium | Medium | Flexible access |

When Should You Use Your Emergency Fund?

You should use your emergency fund only for serious, necessary, and unexpected situations. Valid reasons include job loss, medical emergencies, urgent home repairs, important car repairs, or sudden family needs. These events can affect your health, income, safety, or basic living needs. This Emergency Fund Guide helps you understand that the money exists to protect you from financial pressure and expensive debt.

You should not use this money for vacations, shopping, parties, gadgets, or lifestyle upgrades. Those are wants, not emergencies. Before spending from the fund, ask yourself if the cost is urgent, important, and unexpected. If it is not, keep the money protected for real emergencies. This discipline keeps your safety fund strong and available when timing truly matters.

Common Mistakes to Avoid in Your Emergency Fund Guide

Many people make mistakes that slow down their progress. One common mistake is saving too little or saving without a clear goal. Another mistake is using the fund for non-emergency spending. Some people also invest emergency money in risky assets, which can reduce safety and quick access. That defeats the main purpose of emergency savings and can create stress during urgent situations.

You should also rebuild the fund after using it. If you spend part of your savings, start saving again as soon as possible. Strong financial habits come from discipline, planning, and regular review. This Emergency Fund Guide helps you avoid common errors and protect long-term financial security through better money control and careful saving.

FAQs

How to build an emergency fund quickly?

Start small and save regularly. Automate your savings, reduce unnecessary expenses, and use extra income to grow your emergency fund faster.

Is a 3 month emergency fund enough?

Yes, a 3 month emergency fund can be enough if your income is stable. If your income is uncertain, self-employed, or commission-based, a 6 month emergency fund is safer.

Should I invest my emergency savings?

No, emergency savings should stay safe and easy to access. Avoid risky investments because you may need the money quickly during a real emergency.

Where is the safest place to keep an emergency fund?

A savings account or high-yield savings account is usually a safe option. These accounts keep your money accessible while helping you separate emergency money from daily spending.

How do I calculate my emergency fund amount?

Add your essential monthly expenses, including rent, food, bills, transport, and insurance. Then multiply that amount by 3 or 6 based on your income stability and lifestyle.

Conclusion

This Emergency Fund Guide shows that financial security starts with simple, consistent action. You need a clear savings goal, a realistic savings plan, and a safe place to keep emergency savings. Whether you begin with a small amount or aim for a 3 month emergency fund, steady progress matters most.

Start building your financial safety net today. Emergency savings can protect you from debt, reduce stress, and give confidence during uncertain times. With patience and discipline, this Emergency Fund Guide can support long-term financial security and better money decisions. For support or publishing inquiries, visit the Contact USA Top Guest Post Site page.