Strong credit utilization ratio tips help you manage credit with confidence from the beginning. You learn what credit utilization means and why lenders care about your balances. You also see how simple habits can improve credit score results over time. We explain practical credit card balance management steps for everyday U.S. cardholders. Use these credit health tips to build better control, reduce stress, and protect your future borrowing power.

What Is Credit Utilization Ratio and How Does It Affect Your Credit Score?

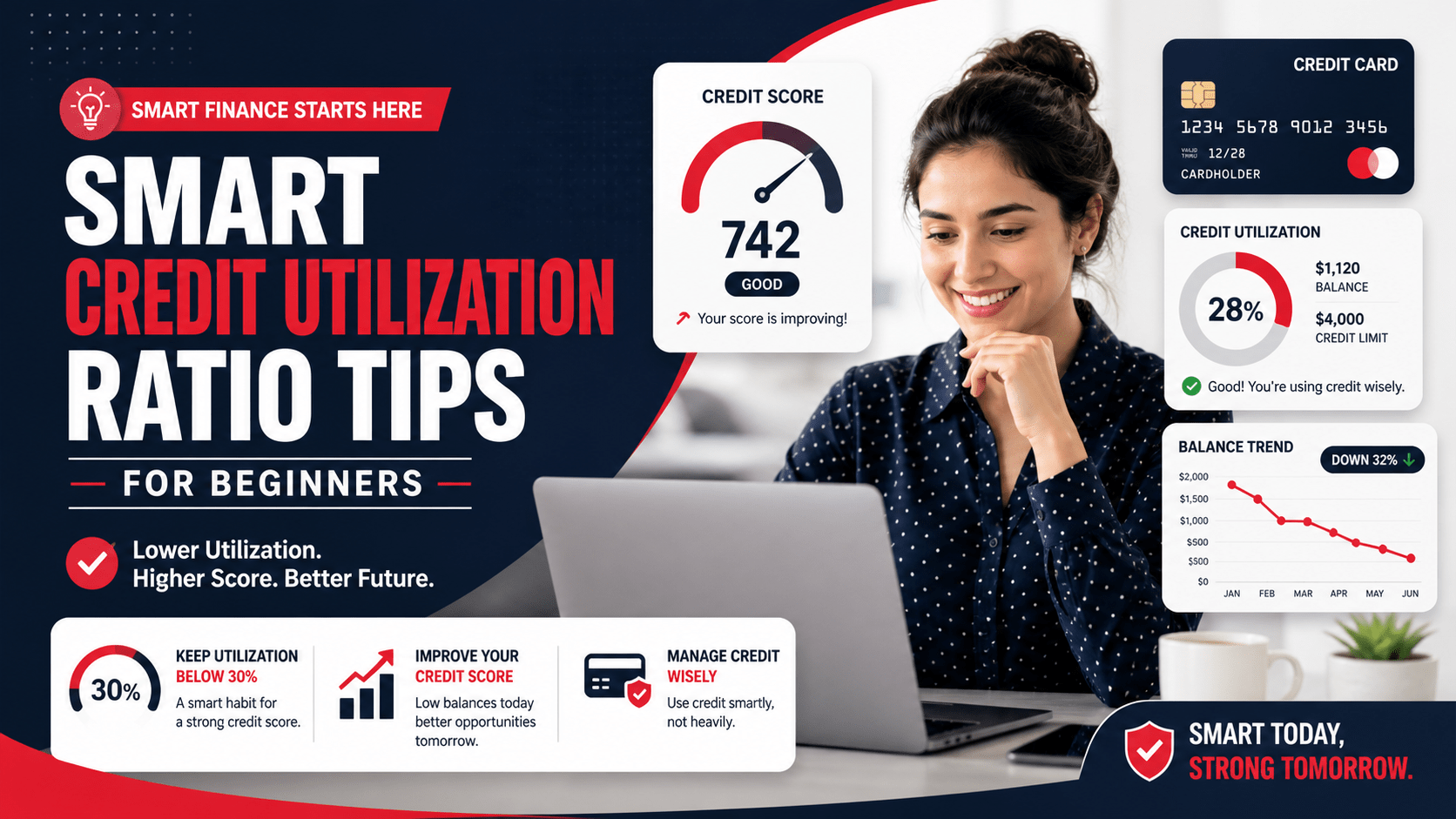

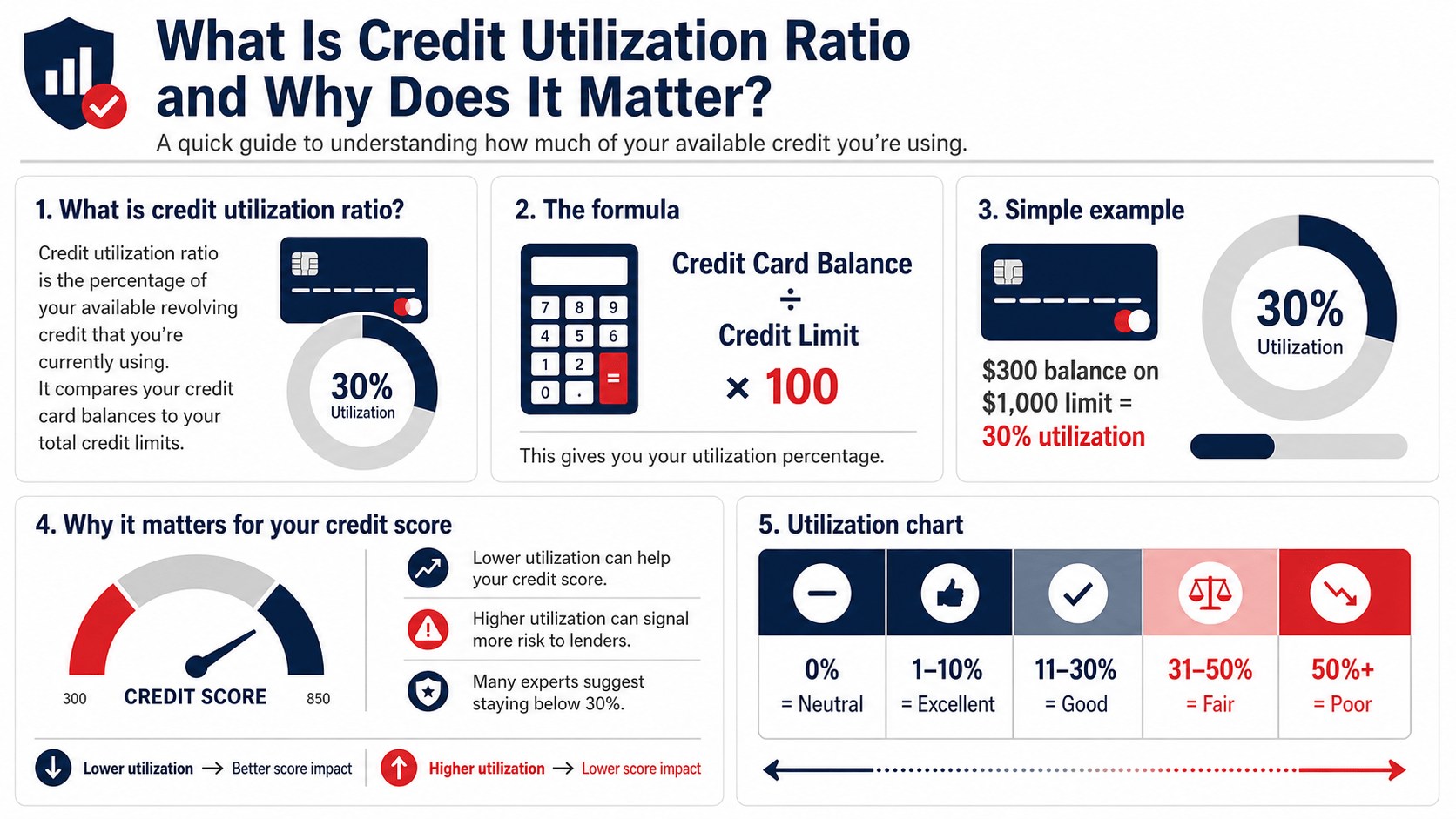

Your credit utilization ratio shows how much available revolving credit you use. It compares your credit card balances with your credit limits. Many lenders review this number because it reveals spending control. You may also hear people call it a debt utilization ratio. It connects closely with major credit score factors, especially the amounts you owe on credit cards.

High utilization can make lenders see more risk in your profile. Lower utilization can show that you borrow with discipline and plan payments well. In our experience, beginners often chase payment history only. Payment history matters, but smart credit utilization ratio tips also help you improve credit score results faster. For more simple money guidance, you can explore our guide on personal finance tips usa.

How to Calculate Your Credit Utilization Ratio Correctly

You can calculate your ratio with one simple formula. Calculate your credit utilization by dividing the sum of your credit card balances by your total available credit limits. Then multiply the result by one hundred. This calculation helps you plan stronger credit card balance management and understand your real borrowing pattern.

- Add every credit card balance you currently carry.

- Add every credit limit available across your cards.

- Compare each card balance with that card limit.

- Track both individual card usage and total usage.

- Check statement dates before you make large payments.

- Use card apps or budgeting tools to monitor balances.

For example, three hundred dollars on a one thousand dollar limit equals thirty percent utilization. If you carry two cards, check both cards separately. One high card can still hurt your profile. Review balances before statement close, not only before due dates. When you know your numbers, you can apply credit utilization ratio tips with confidence and avoid unnecessary score drops. You can also use Budgeting Tips for Beginners to control spending better.

Why Credit Utilization Ratio Matters More Than You Think

Credit utilization matters because lenders want proof of control. A high card balance can suggest financial pressure, even when you pay on time. A low balance can show that you use credit carefully. Credit score models often consider how much debt you carry compared with available credit. That makes utilization one of the credit score factors you should track closely.

You do not need perfect habits to improve credit score results. You need steady balance control. Many experts suggest keeping utilization below thirty percent, while lower single-digit use can support stronger profiles. Small payment changes can create visible progress when issuers update balances. If your goal includes better savings, our guide on how to save money fast can help you support this habit.

| Utilization Level | Credit Score Impact |

| Zero percent | Neutral because it shows little recent card activity |

| One to ten percent | Excellent for strong credit control |

| Eleven to thirty percent | Good for most beginner profiles |

| Thirty-one to fifty percent | Fair and needs quick attention |

| Over fifty percent | Poor because lenders may see higher risk |

Better credit card balance management turns these numbers into useful action.

Proven Credit Utilization Ratio Tips to Improve Credit Score Fast

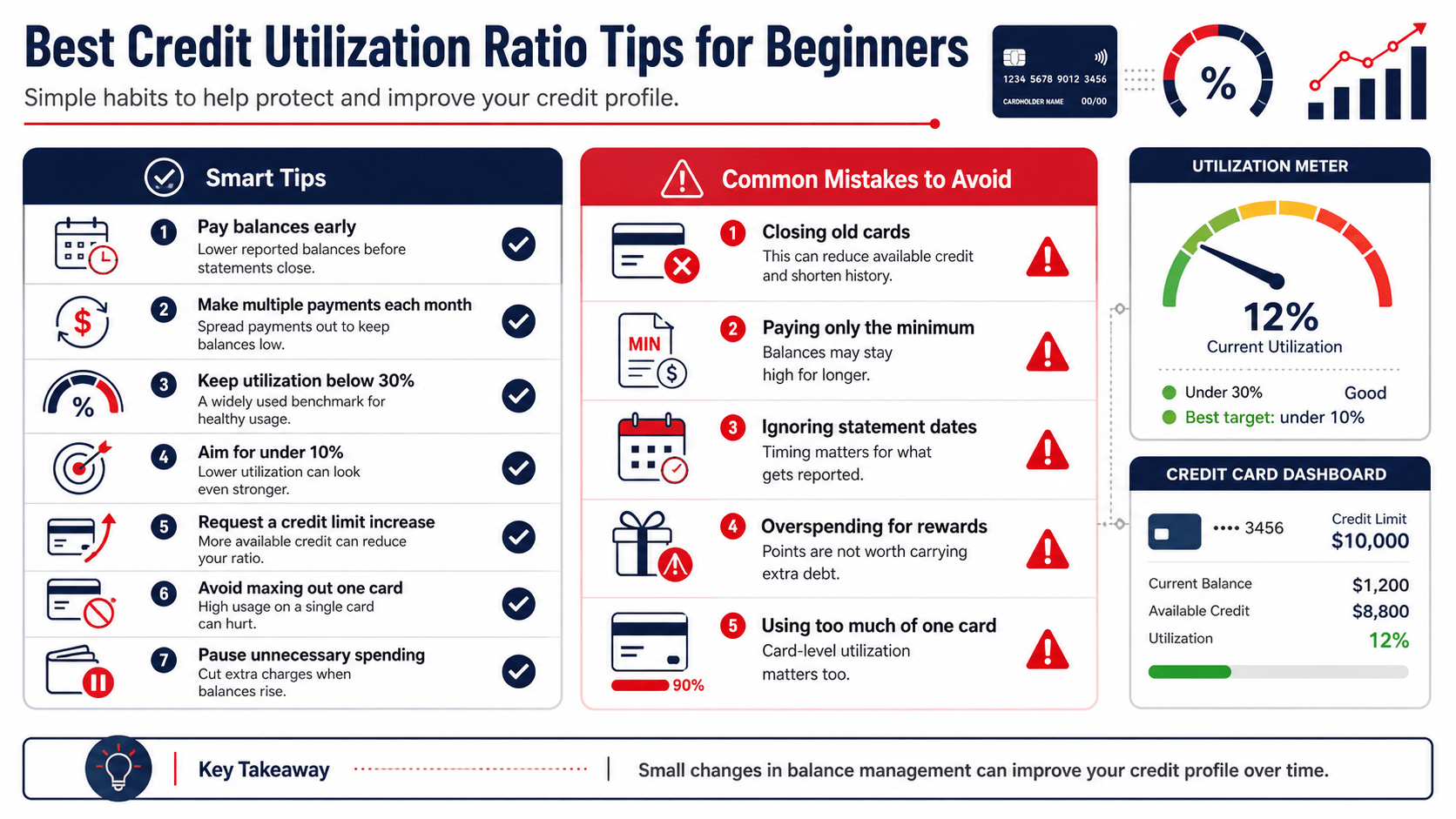

These credit utilization ratio tips help you take practical steps without confusion. You can use them even when your income feels tight. Start with the actions that lower reported balances first. In our experience, small payment changes often help beginners feel more in control.

- Pay balances before your statement closing date.

- Make more than one payment during each billing cycle.

- Keep every card balance below thirty percent of its limit.

- Aim below ten percent when you want stronger results.

- Request a credit card limit increase if your spending stays controlled.

- Avoid maxing out any single card, even for rewards.

- Pause extra spending while you reduce credit card debt.

These credit score tips work best when you repeat them monthly. We often recommend early payments first because they give quick control. You lower what lenders may see, and you build better habits at the same time. If you want more practical savings ideas, read our guide on money saving tips for Americans. Over time, consistent action can help you improve credit score results and reduce financial stress.

Advanced Credit Card Balance Management Strategies Most Beginners Miss

Most beginners focus only on the due date. That protects you from late fees, but it may not lower the balance that reaches your credit report. You should learn your statement closing date and plan payments before that date.

You can also create a personal spending cap below your real card limit. For example, you may treat a one thousand dollar limit like a three hundred dollar limit. This simple rule supports a healthier debt utilization ratio and prevents careless spending.

Budgeting makes these strategies stronger. When you review spending weekly, you catch problems early. We recommend pairing utilization tracking with a simple budget because it turns credit health tips into daily behavior. This approach also helps U.S. consumers handle gas, groceries, subscriptions, and online purchases without balance shock.

| Strategy | Benefit |

| Early payments | Lowers reported balance |

| Multiple payments | Improves utilization control |

| Spending tracking | Prevents overspending |

| Limit increases | Improves available credit |

Advanced credit utilization ratio tips work because timing matters as much as payment amount. You gain control before balances become credit problems. You also build discipline that supports Financial independence tips and long-term borrowing confidence.

Common Mistakes That Hurt Your Credit Utilization Ratio

Many beginners hurt utilization through small mistakes. Closing old cards can reduce your available credit and raise your ratio. Paying only minimum balances can keep debt high for too long. Ignoring statement dates can also make lenders see larger balances than you expect.

Poor credit card balance management can block your plan to improve credit score results. You should avoid maxed-out cards, rushed applications, and emotional spending. These habits affect credit score factors and may limit approvals for cars, apartments, or mortgages. A simple review each week can help you catch problems before they damage your credit health. Better credit habits can also prepare you for future goals like how to start investing in the US.

How to Maintain a Healthy Credit Utilization Ratio Long-Term

You maintain a healthy ratio through steady habits. Check balances often and keep spending below your comfort level. Pay early when possible. These actions help your credit utilization ratio tips keep working after your score improves. You should also review every card before large purchases.

You should treat credit as a tool, not extra income. Use cards for planned purchases only. Track your debt utilization ratio every month. Build a small emergency fund so you do not lean on cards during every surprise. With patience, these credit health tips can support stronger credit choices for years. You can also explore beginner investing tips once your credit and budget feel stable.

FAQs

How much does credit utilization affect your credit score?

It plays a major role among credit score factors. Lower utilization can help you improve credit score results when you also pay on time.

What is the ideal credit utilization ratio?

Many experts suggest staying below thirty percent. A lower range, especially below ten percent, may support stronger credit health.

Does paying off my credit card immediately help?

Yes. Early payments improve credit card balance management and may lower your reported balance.

Will increasing my credit limit improve my score?

A credit card limit increase can help when your spending stays the same. It raises available credit and lowers utilization.

Can I improve my score without paying off all debt?

Yes. Smart credit utilization ratio tips, lower balances, and better payment timing can help you make progress. For more helpful guides, visit the USA Top Guest Post Site Home page.

Conclusion

Smart credit utilization ratio tips can help you improve credit score results and build financial stability. You do not need extreme changes. You need steady tracking, early payments, and better credit card balance management. These actions can help you reduce credit card debt and protect your credit profile. Once you build control, you can explore long term investing strategies for future growth.

At USA Top Guest Post Site Services, we believe useful finance content should guide real decisions. Keep your utilization low, avoid common mistakes, and follow proven credit health tips. You can learn more about us on the About Us Page. For SEO-focused finance content, contact USA Top Guest Post Site through our Contact Us Page or email info@usatopguestpostsite.org today.

Related Helpful Resources